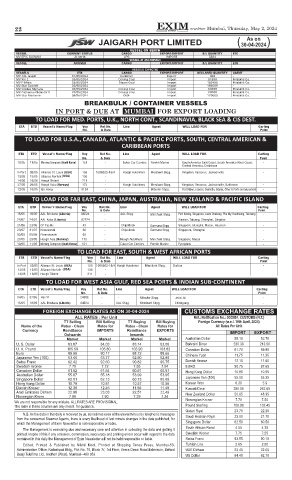

Page 22 - MUMBAI - 10 MARCH 2025

P. 22

18 EXIM newsletter Mumbai & Western India, Monday, March 10, 2025

INDIA

Baltic Exchange Market Report (7 March 2025)

From page 6 nas/US Gulf route (TD9) had 10 points clipped from a week

$403.571. ago and are now at WS132.78 (showing a daily round-trip TCE

Handymax of about $25,687) and WS130.94 (which shows a daily round-

Baltic Clean Handymax routes diverged this week. In the trip TCE of $24,833), respectively.

Mediterranean, the TC6 index had a late week boost jumping The rate for the transatlantic route of 70,000 mt US Gulf/

33.33 points to WS181.11. Up on the UK-Continent, the TC23 UK Continent (TD25) had 15 points deducted and is now at

30kt Cross UK-Continent on the other hand dropped from WS143.89 giving a round-trip TCE basis Houston/Rotterdam

WS199.44 to WS178.33. of $34,447 per day.

VLCC LNG

The market remained steady on the VLCCs this week, with This week, the LNG market continued its positive momen-

the exception of the US Gulf to China route (TD22). The tum, with further rate increases across key routes for 160k cbm

270,000 mt Middle East Gulf to China trip (TD3C) remained and 174k cbm vessels, driven by tightening tonnage availability.

around last week’s levels being assessed on Thursday at WS57.10 On the BLNG1 Gladstone-Tokyo route, 174k cbm vessels

corresponding to a round-trip TCE of $38,342 which is $1,000 recorded a $2,500 increase, bringing rates to $18,200 per day,

more than a week ago. further reinforcing positive sentiment in the Pacific. Mean-

In the Atlantic market, the rate for 260,000 mt West Africa/ while, 160k cbm vessels saw a $1,500 gain, reaching $10,500 per

China (TD15) slipped a single point to WS58.50 giving a round day, continuing the recovery for smaller tonnage.

In the Atlantic, the BLNG2

Sabine-UK Continent route

saw 174k cbm vessels rise by

$1,900, closing at $19,800 per

day, reflecting sustained demand.

Similarly, 160k cbm vessels saw

a $1,200 increase, reaching

$11,100 per day, reinforcing the

market’s upward trajectory.

The BLNG3 Sabine-Tokyo

route showed a slight divergence,

with 174k cbm vessels increasing

voyage TCE of $40,633 per day, an increase of about $500 per by $1,800 to $23,800 per day, while 160k cbm vessels declined

day week-on-week. The rate however for 270,000 mt US Gulf/ by $200, settling at $13,000 per day. This suggests some pressure

China (TD22) collapsed $767,500 over the week and is now at on smaller tonnage earnings despite overall market strength.

$7,280,000, which shows a daily round-trip TCE of $36,497 The term market has picked up this week to reflect spot sen-

(about $4,700 per day less than a week ago). timent, with six-month rates rising by $2,150 to $18,150, one-

Suezmax year rates increased by $650 to $23,075, and three-year rates in-

Suezmax owners have tried to pull rates back up this week. creased by $2,750 to $49,500.

The rate for the 130,000 mt Nigeria/UK Continent voyage With rates continuing their upward trajectory, particularly in

(TD20) rose 2.5 points to WS87.83 meaning a daily round-trip the Atlantic, the market remains bullish due to tightening ton-

TCE of $36,548 while the TD27 route (Guyana to UK Conti- nage. However, it will be interesting to see whether this trend

nent basis 130,000 mt) rose a point to WS85.83 translating into persists or if it is merely a dead cat bounce. As more redeliveries

a daily round-trip TCE of $35,061 basis discharge in Rotter- re-enter the market, rates may revert to their previous levels.

dam. For the TD6 route of 135,000 mt CPC/Med, the rate has LPG

modestly improved by a point to WS100.9. This shows a daily The LPG market has remained static this week, largely due to

TCE of a $39,838 round-trip. In the Middle East, the rate for most market participants being in Tokyo, with only minor fluc-

the TD23 route of 140,000 mt Middle East Gulf to the Medi- tuations across key routes. On the BLPG1 Ras Tanura-Chiba

terranean (via the Suez Canal) rose 1.5 points to a fraction over route, rates increased by $1.25, settling at $46.25. TCE earnings

WS91. followed suit, rising by $2,656 to $29,070.

Aframax In the Atlantic, the BLPG2 Houston-Flushing route expe-

In the North Sea, the rate for the 80,000 mt Cross-UK Con- rienced a $1.00 decline, closing at $48.50. TCE earnings saw a

tinent route (TD7) has eased slightly to between the WS107.5- negligible improvement of $46, reaching $45,171. Meanwhile,

110 level giving a daily round-trip TCE of around $27,000 basis the BLPG3 Houston-Chiba route saw a $2.00 drop in rates, set-

Hound Point to Wilhelmshaven. tling at $92.33. TCE earnings remained stable, with a very small

In the Mediterranean market, the rate for 80,000 mt Cross- decline of $29, closing at $29,604.

Mediterranean (TD19) has been reduced by 3.5 points to Overall, the LPG market saw limited activity this week, with

WS121.28 (basis Ceyhan to Lavera, that shows a daily round- only a few cargoes reported. Once all market participants return

trip TCE of about $29,733, about $1,000 less than a week ago). from Tokyo, we may see a resurgence.

Across the Atlantic, the market has capitulated after a few

stem cancellations and vessel de-scheduling in Mexico adding The BDI increased from 1,229 on February 28,

pressure to owners in the arena. The rate for the 70,000 mt East 2025 to 1,276 on March 3 and 1,286 towards the

Coast Mexico/US Gulf route (TD26) and the 70,000 mt Cove- end of the week.

Disclaimer: While reasonable care has been taken by the Baltic in providing the Materials, all such Materials are for general use,

provided without warranty or representation, is not designed to be used for or relied upon for any specific purpose, and does not infringe

upon the legitimate rights and interests of any third party including intellectual property. The Baltic will not accept any liability for any loss

incurred in any way whatsoever by any person who seeks to rely on the information contained herein. All intellectual property and related

rights in the Materials are owned by the Baltic. Any form of copying, distribution, extraction or re-utilisation of this information by any means,

whether electronic or otherwise, is expressly prohibited. Persons wishing to do so must first obtain a licence to do so from the Baltic.